Caterina Batog, Research & Economics Analyst, British Chambers of Commerce

The Autumn Budget was delivered against a backdrop of a weak economic picture, high borrowing costs and limited fiscal headroom. Although the Chancellor announced measures to improve infrastructure and skills, these are unlikely to offset the deeper structural challenges weighing on the economy. With growth still subdued and productivity flat, the BCC’s latest forecast expects growth outlook to remain subdued, suggesting last month’s Budget is unlikely to kickstart the UK economy.

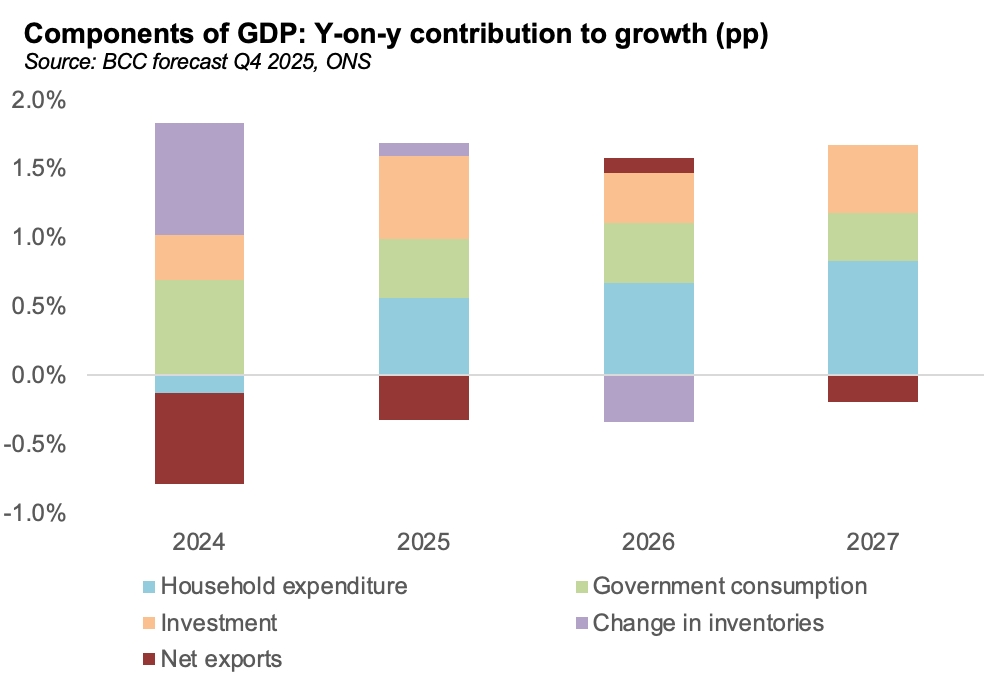

Public spending continues to support growth this year

Our latest economic forecast shows a small upgrade to UK growth this year, from 1.3% to 1.4%, supported by strong public spending throughout 2025. However, for the next two years, we see no major improvement in the economic outlook – growth is expected to be 1.2% in 2026 and 1.5% in 2027, unchanged from previous quarter, reflecting limited productivity gains and the continued effects of cautious fiscal tightening. However, the modest improvement in growth is expected to draw some support from the Budget’s investment-focused approach.

Business investment is projected to remain weak, rising only 0.9% in 2026 and 1.5% in 2027, as a result of weak demand conditions, additional cost pressures reducing margins and continued high uncertainty, causing businesses to delay their investment plans. This combination continues to weigh on business confidence, leading many firms to delay or scale back their investment plans.

Exports are expected to pick up in 2025 by 3% as a result of a strong Q1 but more recently exports growth has slowed, with exports expected to remain weak in the next two years, 1.8% next year and 2.4% in 2027. The reason why exports are looking momentum is because of global demand, particularly in Europe, remains weak and the UK’s trade exposed sectors face tariff challenges.

Inflation is set to continue easing and is forecast to return to the Bank of England’s 2% target by the end of 2027, driven by slower wage growth and softer labour-market conditions. However, risks persist, including pressures from food prices and higher employment costs. With inflation cooling and growth subdued, the BoE is expected to cut interest rates in December 2025, with the bank rate projected to remain at 3.5% through 2026 and 2027.

The labour market is loosening as firms respond to weak sales growth and higher wage costs from earlier inflation. Unemployment is expected to pick up next year by 5.1% as businesses face weak demand and high employment costs. Additionally, businesses have little incentive to expand payrolls, implying future employment gains will be minimal and unemployment may edge higher. Unemployment is then expected to slow down in 2027 to only 4.8%.

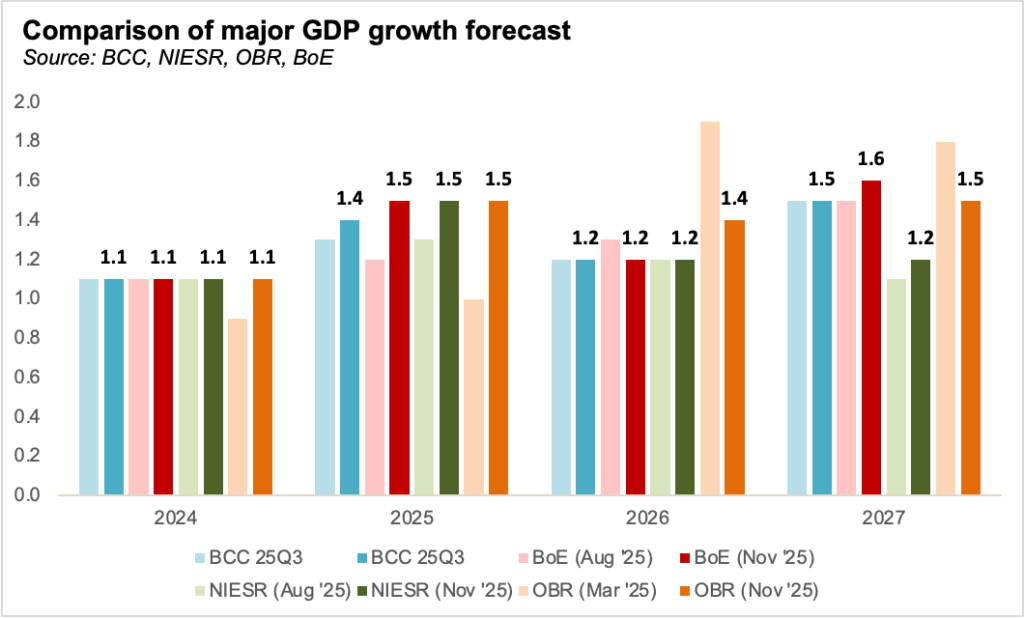

BCC growth forecast remains broadly in line with the BoE and NIESR

The BCC’s forecast for the next year is broadly in line with the November’s BoE and NIESR forecasts projecting 1.2% growth. In comparison, the OBR remains more optimistic forecasting growth of 1.4% in 2026. In 2027 our forecast of 1.5% remains broadly consistent with the BoE and the OBR expecting growth of 1.6% and 1.5%, while NIESR takes a more pessimistic stance at 1.2%. Overall, there is limited differences across the BoE and NIESR, with both expecting only modest growth and the OBR revising its expectations for 2026 and 2027 downward.

Challenges and risks that weight on UK Outlook

The UK continues to face weak consumer demand, driven by squeezed incomes, and frozen tax thresholds. At the same time, the labour market is loosening, with rising unemployment, falling vacancies, and slowing wage growth. With businesses facing weak demand and high employment costs, further job cuts are expected to be seen, meaning labour-market conditions may remain subdued through 2026-27.

Inflation has eased from its peak and is expected to decline further into 2026, but upside risks remain, driven by greater domestically generated inflation and food prices. High US tariffs are adding to global uncertainty and sustaining inflationary pressures, while the lack of a meaningful “reset” in UK-EU trade relations continues to limit clarity and stability for businesses and trade.

The economy also remains vulnerable to unexpected shocks, such as energy price spikes, geopolitical tensions, which could quickly weaken business confidence, impact an already fragile supply chain, raise costs, and further delay the UK’s recovery from the low-growth environment.

How can the UK escape the low-growth trap?

Unlocking UK growth will require a strategic focus on competitiveness, resilience, and trade strength. A clearer long-term framework to support exporters, reduce trade frictions, and attract investment into high-growth industries is crucial. Improving market access, especially with the EU, would help ease cost pressures for firms and address the struggling trade-exposed sectors. By reducing trade barriers, supporting investment, and creating a more predictable business environment, the Government could help shift the UK out of its low-growth trajectory.

AI could also play an important role in boosting productivity, but only if SMEs have the skills and the capacity to use it effectively – without the right knowledge and guidance, firms risk missing out on the benefits AI can offer. That’s why the BCC has launched the AI Academy to equip UK businesses with practical tools, training and confidence to adopt AI.

Further reading:

- BCC’s Economic Forecast https://www.britishchambers.org.uk/news/2025/12/bcc-economic-forecast-budget-unlikely-to-be-growth-game-changer/

- BCC Insights Unit research and publications: https://www.britishchambers.org.uk/insights-unit/publications-and-commentary/